The Short Answer: President Trump signed legislation on July 4, 2025, reducing the $200 NFA tax stamp to $0 for suppressors, SBRs, SBSs, and AOWs starting January 1, 2026. Multiple Second Amendment organizations have filed federal lawsuits arguing that the remaining NFA registry is unconstitutional without the tax. Courts have not yet ruled on these claims.

For federal firearms licensees (FFLs), the National Firearms Act (NFA) has represented both opportunity and regulatory burden since 1934. The recent elimination of the $200 tax stamp on suppressors, short-barreled rifles, short-barreled shotguns, and “any other weapons” marks the most significant NFA reform in nearly a century. However, this change brings new legal challenges that could reshape how FFLs handle NFA transfers.

The One Big Beautiful Bill Act, signed July 4, 2025, removes the financial barrier while preserving the registration process. This compromise has triggered multiple federal lawsuits challenging the entire constitutional foundation of the NFA. Understanding these developments is important for FFLs navigating evolving compliance requirements.

Understanding the NFA Tax Stamp Changes

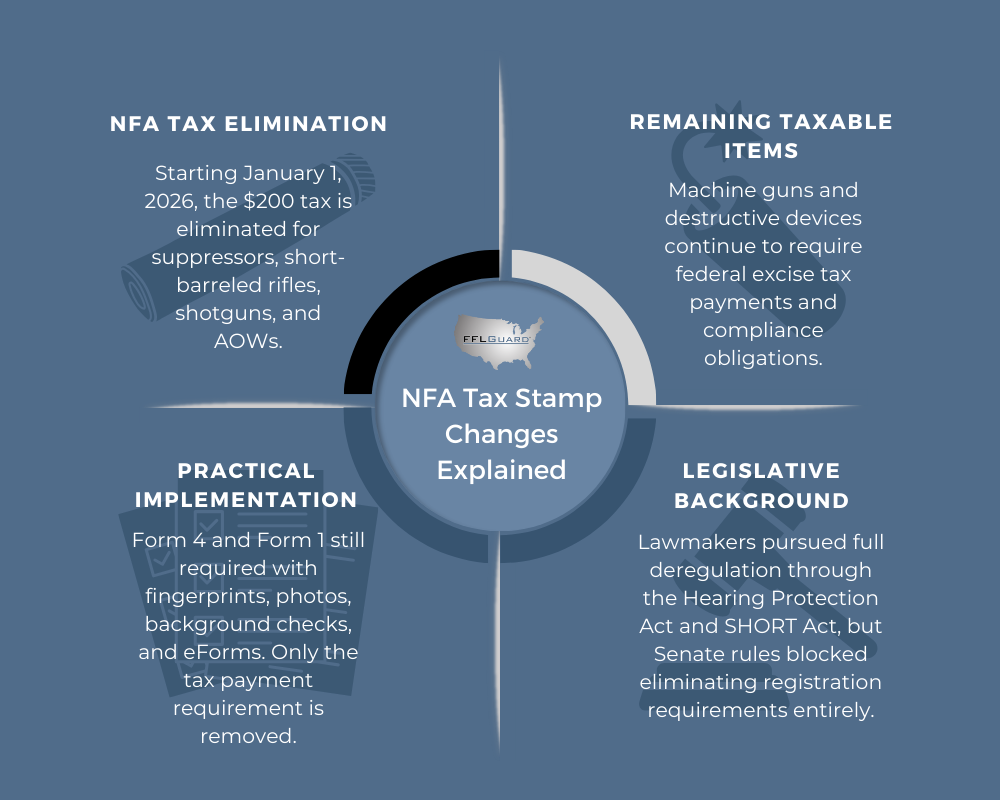

The tax elimination affects specific categories under the NFA. Starting January 1, 2026, transfers and manufacturing of suppressors, short-barreled rifles, short-barreled shotguns, and AOWs will no longer require the $200 federal excise tax. Machine guns and destructive devices remain subject to existing taxation.

Legislative Background

Republican lawmakers originally planned complete NFA deregulation through the Hearing Protection Act and SHORT Act provisions. These measures would have removed affected items from NFA oversight entirely, treating suppressors like standard firearms under the Gun Control Act (GCA). The Senate Parliamentarian blocked comprehensive reforms under the Byrd Rule, determining that eliminating registration requirements constituted policy changes beyond the reconciliation scope. The final legislation, H.R. 1 (the One Big Beautiful Bill Act), passed the Senate on July 4, 2025.

Practical Implementation

Bureau of Alcohol, Tobacco, Firearms and Explosives (ATF) Form 4 and Form 1 applications continue unchanged except for the tax payment requirement. However, there are pending updates to these documents which, in addition to other changes, include the elimination of the $200 tax payment for SBRs, SBSs, suppressors, and AOWs. FFLs must still process a fingerprint card, photographs, background checks, and other documentation necessary for these ATF forms. Wait times remain subject to current processing schedules, though increased demand may extend approval periods.

The demand for suppressors and short-barreled firearms will increase once the tax disappears. FFLs should prepare for increased customer inquiries and potential inventory challenges as manufacturers adjust to higher demand.

Constitutional Legal Challenges

The elimination of NFA taxation has created what constitutional scholars view as a potential vulnerability. Multiple Second Amendment organizations argue that without revenue generation, the remaining NFA framework lacks proper constitutional authorization.

The Taxing Power Foundation

In Sonzinsky v. United States (1937), the Supreme Court upheld the NFA specifically under Congress’s Article I taxing power. The Court ruled the law remained constitutional as a tax measure despite secondary regulatory effects. Gun rights advocates now argue this constitutional foundation has collapsed without actual revenue generation—though this is an argument, not an established legal conclusion.

Legal challenges also draw parallels to the Affordable Care Act’s mandate. When Congress reduced that tax to $0, some courts ruled the mandate could no longer be justified under taxing authority, though the Supreme Court ultimately dismissed that case on standing grounds without adopting the theory. Plaintiffs are advancing similar arguments here.

Current Federal Lawsuits

Gun Owners of America Coalition: Filed in the Northern District of Texas on July 4, 2025, this lawsuit includes Palmetto State Armory, Silencer Shop Foundation, Firearms Regulatory Accountability Coalition, B&T USA, and SilencerCo. The case seeks declarations that NFA registration requirements exceed congressional enumerated powers and injunctions preventing ATF enforcement on untaxed items.

Multi-Organization Alliance: The National Rifle Association, American Suppressor Association, Firearms Policy Coalition, and Second Amendment Foundation announced a joint federal lawsuit challenging NFA constitutionality. This separate legal challenge focuses on similar constitutional arguments about congressional authority without taxation.

Both cases argue that Article I provides no alternative constitutional basis for NFA registration and transfer restrictions once the revenue-generating tax is eliminated.

Political Response and Counter-Measures

Democratic lawmakers have responded aggressively to NFA tax elimination. Senator Chris Murphy of Connecticut introduced Senate Amendment 2973 in July 2025, proposing to raise the transfer tax from $0 to $4,709 per item.

The $4,700 Tax Proposal

Murphy’s amendment would increase AOW taxes from $5 to $55 and strike existing tax-related language from federal tax code. Gun control organizations praised the proposal, claiming it adjusts the 1934 tax rate for current inflation. However, the amendment faced significant procedural obstacles and is not expected to advance in the Republican-controlled Senate.

The proposal would likely be subject to a Senate Standing Rule XVI point of order, which requires amendments to be relevant to underlying appropriations bills. The Military Construction, Veterans Affairs, and Related Agencies Appropriations Act contains no firearms-related provisions, making Murphy’s NFA amendment procedurally improper.

State-Level Implications

Many states condition suppressor, SBR, and/or SBS legality on compliance with federal NFA status. If courts strike down NFA requirements, these states would need new legislation addressing ownership and transfer. Some states may respond by tightening restrictions or bans if federal oversight disappears.

FFLs operating in multiple states should monitor local legislative responses to potential NFA changes. State compliance requirements may diverge significantly from federal standards depending on court outcomes.

Impact on Federal Firearms Licensees and Market Outlook

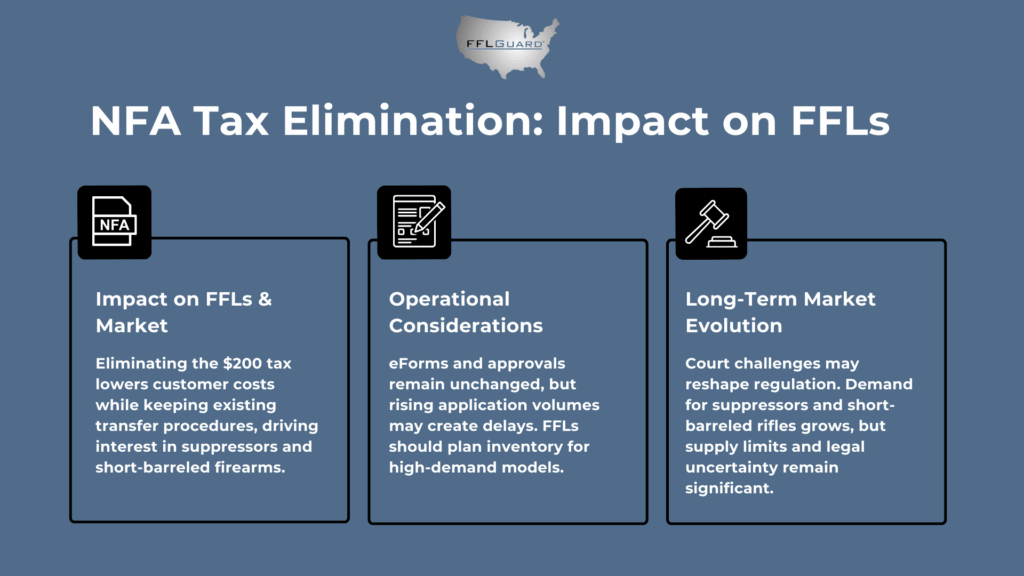

The $0 tax represents immediate changes for FFL operations. Eliminating the $200 fee removes a significant customer cost barrier while preserving existing transfer procedures. FFLs can expect increased interest in suppressors and short-barreled firearms as financial obstacles disappear.

Operational Considerations

Current eForms processing continues unchanged, requiring the same documentation and approval procedures. FFLs should prepare for potential processing delays as application volumes increase. Demand is expected to rise sharply when the cost barrier is removed, though exact increases vary by forecast.

Inventory management becomes increasingly important as manufacturers may struggle to meet initial demand surges. FFLs should consider advance planning for popular suppressor and short-barreled rifle models.

Customer Decision Points

Prospective buyers face timing decisions between purchasing now with current $200 taxes or waiting until January 2026. Buying immediately means faster possession but higher costs, while waiting saves money but likely means longer approval queues and potential supply shortages.

FFLs should educate customers about these trade-offs while avoiding specific tax advice. The choice depends on individual priorities regarding cost savings versus possession timing.

Long-Term Legal and Market Evolution

Legal challenges could take years to resolve through federal appeals courts, with potential Supreme Court involvement. Even favorable lower court rulings may face stays during appeals, limiting immediate practical changes beyond tax elimination.

Suppressor manufacturers anticipate substantial demand increases but face production capacity limitations. The short-barreled rifle market may experience similar growth as barriers decrease. FFLs should consider customer education about realistic delivery timeframes.

If legal challenges succeed in eliminating NFA requirements entirely, the regulatory landscape would shift dramatically. Suppressors and short-barreled firearms would potentially transfer like standard firearms through Form 4473 and background / NICS checks only.

FFLGuard: Your Partner in NFA Compliance Navigation

The federal government’s elimination of the tax stamp fee through the reconciliation bill represents a historic shift for suppressor ownership and NFA firearm regulations. Starting January 2026, the application process for NFA items, including suppressors, short-barreled rifles, and other NFA weapons, will no longer require the traditional $200 payment, though registration and transfer requirements remain intact. This significant change affects law enforcement procedures, dealer operations, and customer decisions across the firearms industry.

As federal courts review constitutional challenges to the remaining NFA framework, FFLs must navigate evolving compliance requirements while preparing for increased demand in NFA item transfers. FFLGuard provides essential guidance through these regulatory transitions, ensuring your business maintains full compliance as the landscape for NFA weapons and suppressor ownership continues to evolve.

And, don’t forget, the ATF Forms associated with NFA items will be changing. Keep a close eye on the release and use by dates for the updated documents, because – once ATF has issued a new form – all previous editions are obsolete and will likely be rejected.

Whether managing current NFA processes, preparing for tax elimination implementation, or adapting to potential future regulatory changes, FFLGuard offers the expertise FFLs need by helping FFLs navigate these legal changes while serving customers’ evolving needs in a shifting regulatory environment.

Partner with FFLGuard today to ensure your FFL operations remain compliant and competitive as the firearms industry adapts to these historic regulatory changes.